Creditas Releases its Q3-2025 Results and Financial Statements

28 november, 2025

28 november, 2025

Creditas Releases its Q3-2025 Results and Financial Statements

We continue accelerating sustainable growth, balancing gross profit generation and investments in customer acquisition, automation and our artificial intelligence platform

Business Context

Key Highlights – Q3 2025

Portfolio

Financials

Operations

Third Quarter Financial & Operating Results

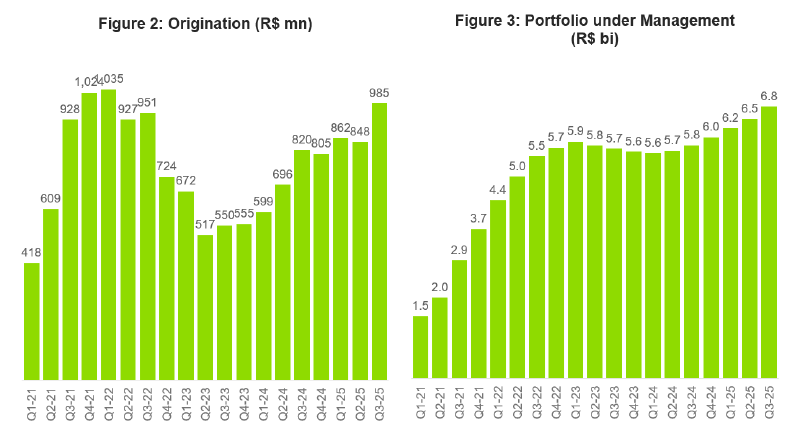

In Q3-2025, we maintained our focus on profitable growth, achieving solid results in all our verticals. Origination increased 20% and our Portfolio grew 17% YoY (see Figure 2 and 3). This origination performance is the strongest since 2021, marking a significant milestone: we now achieve this level of growth with a clear focus on profitability and substantially higher operational productivity, contrasting sharply with the volume growth focus of the 2020-2021 period.

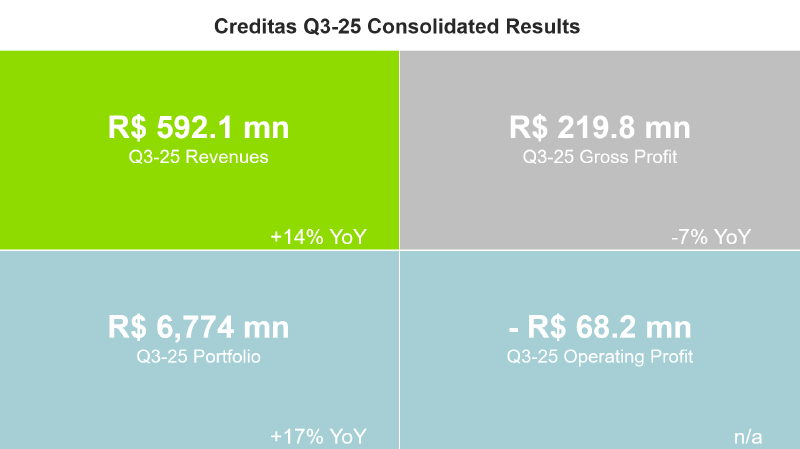

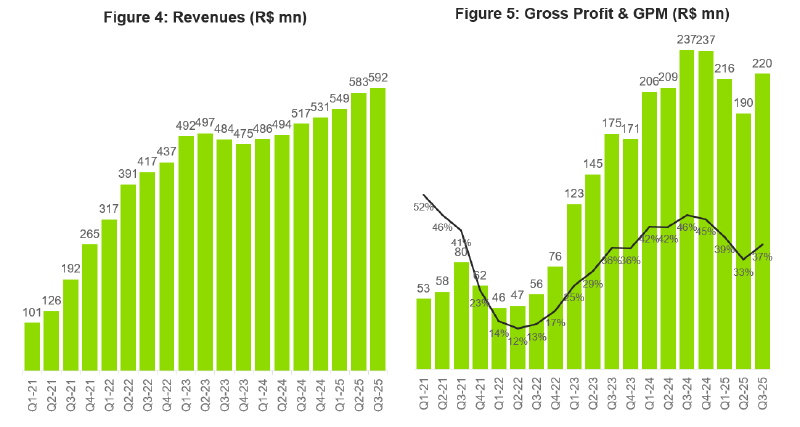

The continued increase in Portfolio supported revenues growth to a new record of R$592.1mn in Q3-25 +14.4% YoY (see Figure 4). Gross Profit reached R$219.8 million, delivering a strong 15.6% QoQ increase. This substantial nominal growth was primarily fueled by the continued expansion of our revenue base coupled with improvements in cost of credit. The Gross Profit Margin stood at 37.1%, increasing from 32.6% in Q2-25. Our gross profit margins remain below our cohort profit margins due to two factors: (i) the consolidation of higher SELIC rates in the securitizations’ funding (an effect expected to normalize as the CDI converges with long-term rates –which are currently below short-term rates –and aligns with the swap rate embedded in the portfolio pricing); and (ii) IFRS accounting that front-loads expected losses recognition. Crucially, Profitability at the cohort level remains well above our 40% target, allowing us to sustain our growth strategy despite the short-term accounting impact on the gross profit margin (See Figure 5).

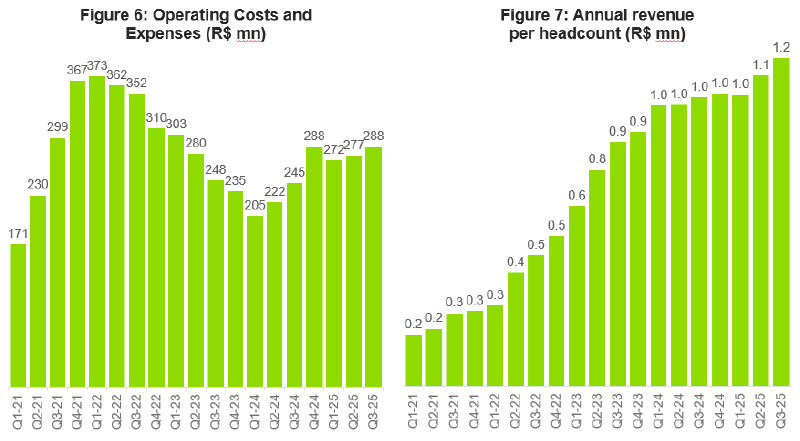

Costs below gross profit (see Figure 6) reached R$288mn in the quarter, a modest 3.8% QoQ increase, primarily due to growth-related CAC expenses and one-off funding vehicles’ costs. The rise in CAC was directly linked to the acceleration of origination, which returned to historical highs. Growth is now achieved more efficiently with CAC increasing by 6.7% QoQ compared to a much larger 16.1% increase in total origination. Increased productivity through automation and AI together with more successful CRM and affiliates marketing is allowing us to increase IRRs. Productivity measured as Revenues per employee are reaching new highs with R$1.2mn revenues per employee (as a reminder, Creditas has almost all its functions internalized, contrary to market practices that tend to outsource certain core functions like technology, collections or sales). These results demonstrate our ability to achieve significant gains in scale and sustainable value generation. It is important to remember that Creditas recognizes all acquisition and technology costs upfront, while loan and insurance margins accrue over time.

Our focus continues to be on reinvesting the profits of our portfolio to drive growth. This strategy is built on strong unit economics and short payback periods. Although the combined effect of higher growth and a rising SELIC rate impactsshort-term profitability due to accounting recognition, we are prioritizing net present value built on superior IRRs to generate strong future cash flows.

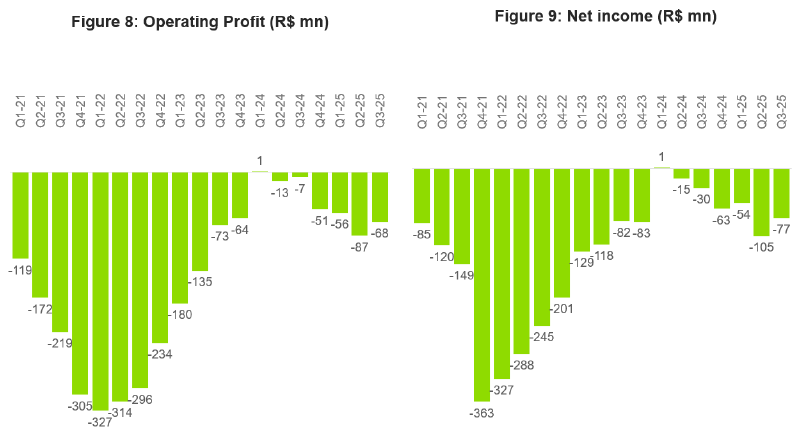

In Q3-25, we recorded an operating loss of R$68.2million (see Figure 8) and a net loss of R$77.1 million (see Figure 9). Importantly, we maintained a neutral cash flow position, which enables us to fund our growth internally without the need for external capital, a key pillar of our long-term strategy. The performance of this quarter highlights our continued momentum and underscores the strength of our discipline in portfolio expansion, cost control and focus on sustainable, long-term value creation.

Business Unit Performance

Auto Equity

The flagship product kept robust origination in Q3-25, sustaining a strong and consistent performance throughout the year. The solid 18% YoY portfolio growth demonstrates the sustained positive impact of our continued investments in digital onboarding and customer acquisition, fueling momentum for Q4-25 and into 2026.

Home Equity

Home Equity delivered record origination in the quarter, building on the strong momentum from 2024 and resulting in 36% YoY portfolio growth. This performance was driven by our strategic focus on improving user experience and lowering acquisition costs, while successfully scaling both our direct-to-consumer and affiliate networks.

Private Employees Payroll Loans

Following increased visibility into the initial unit economics of eConsignado and the normalization of operational processes, we are cautiously increasing origination by progressively expanding our customer coverage (today we are covering less than 6% of the addressable private employee market) while still maintaining a highly selective and cautious approach to risk, prices and volumes.

Auto Finance

After gaining confidence with the product's unit economics and operational experience, we are reaccelerating growth. Our strategic focus on efficiency has been key, leading to our lowest-ever customer acquisition cost and positioning us for a profitable, balanced expansion.

Insurance

We are focusing on the redesign of our user experience as we consolidate Creditas as the largest online broker in Brazil. We are exploring multiple avenues to reach the full potential for insurance within our Creditas ecosystem. We continue investing in these fronts and expect insurance to become instrumental in the growth of our platform over the years.

Business Outlook

Creditas is in a new growth phase, supported by a foundation of high client recurrence that supports our revenue base, strong credit performance, and clear product-market fit across all core offerings. We're prioritizing investments in user experience and automation, with AI now delivering tangible value. This positions us for an annual growth target of 25%+ in the coming years while maintaining portfolio profitability.

28 november, 2025

Creditas Releases its Q3-2025 Results and Financial Statements

We continue accelerating sustainable growth, balancing gross profit generation and investments in customer acquisition, automation and our artificial intelligence platform

Business Context

Key Highlights – Q3 2025

Portfolio

Financials

Operations

Third Quarter Financial & Operating Results

In Q3-2025, we maintained our focus on profitable growth, achieving solid results in all our verticals. Origination increased 20% and our Portfolio grew 17% YoY (see Figure 2 and 3). This origination performance is the strongest since 2021, marking a significant milestone: we now achieve this level of growth with a clear focus on profitability and substantially higher operational productivity, contrasting sharply with the volume growth focus of the 2020-2021 period.

The continued increase in Portfolio supported revenues growth to a new record of R$592.1mn in Q3-25 +14.4% YoY (see Figure 4). Gross Profit reached R$219.8 million, delivering a strong 15.6% QoQ increase. This substantial nominal growth was primarily fueled by the continued expansion of our revenue base coupled with improvements in cost of credit. The Gross Profit Margin stood at 37.1%, increasing from 32.6% in Q2-25. Our gross profit margins remain below our cohort profit margins due to two factors: (i) the consolidation of higher SELIC rates in the securitizations’ funding (an effect expected to normalize as the CDI converges with long-term rates –which are currently below short-term rates –and aligns with the swap rate embedded in the portfolio pricing); and (ii) IFRS accounting that front-loads expected losses recognition. Crucially, Profitability at the cohort level remains well above our 40% target, allowing us to sustain our growth strategy despite the short-term accounting impact on the gross profit margin (See Figure 5).

Costs below gross profit (see Figure 6) reached R$288mn in the quarter, a modest 3.8% QoQ increase, primarily due to growth-related CAC expenses and one-off funding vehicles’ costs. The rise in CAC was directly linked to the acceleration of origination, which returned to historical highs. Growth is now achieved more efficiently with CAC increasing by 6.7% QoQ compared to a much larger 16.1% increase in total origination. Increased productivity through automation and AI together with more successful CRM and affiliates marketing is allowing us to increase IRRs. Productivity measured as Revenues per employee are reaching new highs with R$1.2mn revenues per employee (as a reminder, Creditas has almost all its functions internalized, contrary to market practices that tend to outsource certain core functions like technology, collections or sales). These results demonstrate our ability to achieve significant gains in scale and sustainable value generation. It is important to remember that Creditas recognizes all acquisition and technology costs upfront, while loan and insurance margins accrue over time.

Our focus continues to be on reinvesting the profits of our portfolio to drive growth. This strategy is built on strong unit economics and short payback periods. Although the combined effect of higher growth and a rising SELIC rate impactsshort-term profitability due to accounting recognition, we are prioritizing net present value built on superior IRRs to generate strong future cash flows.

In Q3-25, we recorded an operating loss of R$68.2million (see Figure 8) and a net loss of R$77.1 million (see Figure 9). Importantly, we maintained a neutral cash flow position, which enables us to fund our growth internally without the need for external capital, a key pillar of our long-term strategy. The performance of this quarter highlights our continued momentum and underscores the strength of our discipline in portfolio expansion, cost control and focus on sustainable, long-term value creation.

Business Unit Performance

Auto Equity

The flagship product kept robust origination in Q3-25, sustaining a strong and consistent performance throughout the year. The solid 18% YoY portfolio growth demonstrates the sustained positive impact of our continued investments in digital onboarding and customer acquisition, fueling momentum for Q4-25 and into 2026.

Home Equity

Home Equity delivered record origination in the quarter, building on the strong momentum from 2024 and resulting in 36% YoY portfolio growth. This performance was driven by our strategic focus on improving user experience and lowering acquisition costs, while successfully scaling both our direct-to-consumer and affiliate networks.

Private Employees Payroll Loans

Following increased visibility into the initial unit economics of eConsignado and the normalization of operational processes, we are cautiously increasing origination by progressively expanding our customer coverage (today we are covering less than 6% of the addressable private employee market) while still maintaining a highly selective and cautious approach to risk, prices and volumes.

Auto Finance

After gaining confidence with the product's unit economics and operational experience, we are reaccelerating growth. Our strategic focus on efficiency has been key, leading to our lowest-ever customer acquisition cost and positioning us for a profitable, balanced expansion.

Insurance

We are focusing on the redesign of our user experience as we consolidate Creditas as the largest online broker in Brazil. We are exploring multiple avenues to reach the full potential for insurance within our Creditas ecosystem. We continue investing in these fronts and expect insurance to become instrumental in the growth of our platform over the years.

Business Outlook

Creditas is in a new growth phase, supported by a foundation of high client recurrence that supports our revenue base, strong credit performance, and clear product-market fit across all core offerings. We're prioritizing investments in user experience and automation, with AI now delivering tangible value. This positions us for an annual growth target of 25%+ in the coming years while maintaining portfolio profitability.

Aktieanalys

Aktieanalys

1 DAG %

Senast

OMX Stockholm 30

0,42%

(vid stängning)

Stockholmsbörsen

31 juli, 17:53

Stockholmsbörsen stänger uppåt

Apple

31 juli, 14:50

Apple faller över 7% i förhandeln

OMX Stockholm 30

1 DAG %

Senast

3 246,92